In this guide, we will analyze the specific financial structures that allow you to maximize this seasonal cash flow. We will cover the exact costs you must anticipate, the timeline for deployment, and how to safeguard your investment against inflation.

Visual summary: The comic series below walks through the story and ideas in this article.

📖

Page 1 of 5Nairobi Returns: The Liquidity Trap

In this article, we will cover:

- The Real Cost of Acquisition

- When It Makes Sense to Buy

- The Financing Landscape

- Non-Obvious Capital Tips

- Your Next Move

March 2026 Market Opportunity Snapshot

✨

Liquidity Flow

High (Refund Season)

Strategic ImplicationIdeal for lump-sum down payments

✨

Inventory

Stabilized

Strategic ImplicationPremium units currently available

✨

Price (2BR)

$110k - $160k

Strategic ImplicationEntry point for high-yield rentals

✨

Competition

Rising

Strategic ImplicationSpeed of execution is vital

The Real Cost of Acquisition

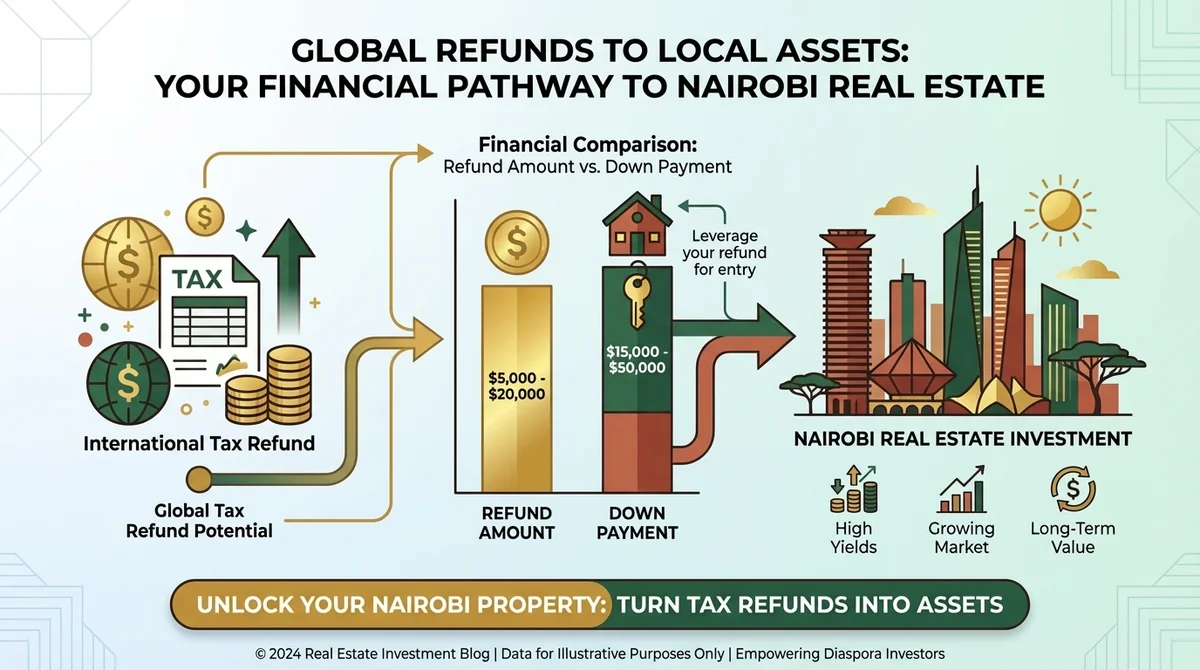

For many in the diaspora, March represents a critical financial window. As tax refunds hit bank accounts in the US, UK, and Canada, smart investors aren't just looking at extra cash—they are calculating how to convert that liquidity into hard assets back home. However, a common pitfall is focusing solely on the listing price. To truly capitalize on this "March Liquidity Boost," you must calculate the total capital required to close a deal in Nairobi.

Initial Capital Requirements for $130,000 Nairobi Apartment

💰Purchase Price

Percentage / RateBase Market Value

Estimated Cost (USD)$130,000

💰Stamp Duty (KRA)

Percentage / Rate4.0% of Value

Estimated Cost (USD)$5,200

💰Legal Fees

Percentage / Rate~1.5% (Est.)

Estimated Cost (USD)$1,950

💰Valuation & Admin

Percentage / Rate~0.5% (Est.)

Estimated Cost (USD)$650

💰Total Cash Needed

Percentage / Rate~106% of Price

Estimated Cost (USD)$137,800

Rehani Soko market data indicates that a standard 2-bedroom apartment in prime Nairobi nodes like Kilimani or Westlands currently trades between $110,000 and $160,000 (KES 14M - 20M). But the sticker price is just the beginning. According to the Kenya Revenue Authority (KRA), Stamp Duty remains fixed at 4% for properties within municipalities and 2% for rural areas. For a $130,000 apartment, that is an immediate $5,200 non-negotiable expense that cannot be financed through a standard mortgage.

Furthermore, ignoring closing costs can derail an otherwise sound investment. Legal fees, governed by the Advocates Remuneration Order, typically range between 1% and 2% of the property value. When you add utility connection fees and potential valuation costs, the "hidden" expenses can easily amount to 6-7% of the purchase price. Our 8-week roadmap eliminates guesswork by factoring these costs in from day one, ensuring your tax refund is allocated efficiently to cover these cash-heavy requirements.

Below is a precise breakdown of the capital required for a typical investment unit.

This data confirms that your tax refund should ideally target these closing costs, preserving your primary capital for the deposit. If you are unsure how your specific refund amount translates into purchasing power, you can run the numbers immediately using our mortgage calculator or consult our AI assistant, Hani, at Ask Hani for a personalized breakdown.

When It Makes Sense to Buy

The decision to deploy capital into real estate should never be impulsive, but March presents a unique window of opportunity. For many investors, particularly those in the diaspora, this period coincides with significant liquidity events—specifically tax refunds. The critical insight is not just having the cash, but deploying it when market inventory is stable and competition is manageable.

According to Rehani Soko market intelligence, property inquiries spike by 15% in Q2, often driving price negotiations harder. acting now allows you to secure assets before this seasonal rush. Buying makes financial sense immediately if your available liquidity covers the "hidden" friction costs of a transaction without depleting your emergency reserves.

For example, purchasing a standard 2BR apartment in an area like Kilimani—priced between $110,000 and $160,000—requires more than just the down payment. You must account for the Kenya Revenue Authority (KRA) stamp duty, which stands at 4% for properties within municipalities, alongside legal fees averaging 1-2%. If your March liquidity injection (tax refund or bonus) can offset these closing costs, your barrier to entry drops significantly. This strategy allows you to preserve your primary capital for the actual deposit, effectively lowering the "pain point" of entry.

Investors should verify their borrowing power before committing. You can run these specific numbers through our mortgage calculator to see exactly how a lump-sum payment impacts your monthly serviceability. If the math shows positive cash flow from day one—where rental income exceeds monthly repayments—the timing is right.

By allocating your refund specifically to closing costs, you effectively reduce your immediate cash requirement by nearly 23%. This approach transforms a tax windfall into a tangible asset, securing a property that Rehani Soko data indicates could yield between 8-11% annually in high-demand zones.

The Financing Landscape

For the Kenyan diaspora, March represents a critical window of opportunity. As tax refunds from the US, UK, and Canada begin to process, smart investors are not viewing this capital as disposable income, but as the cornerstone of their property acquisition strategy. Our 8-week roadmap eliminates guesswork, showing how this annual liquidity event can bridge the gap between aspiration and asset ownership.

Liquidity Impact on Initial Cash Outlay

💰Down Payment (20%)

Estimated Cost ($135,000 Property)$27,000

Refund Strategy ImpactPrimary savings allocation

💰Stamp Duty (4%)

Estimated Cost ($135,000 Property)$5,400

Refund Strategy ImpactCovered by Tax Refund

💰Legal & Admin Fees (~2%)

Estimated Cost ($135,000 Property)$2,700

Refund Strategy ImpactCovered by Tax Refund

💰Total Cash Required

Estimated Cost ($135,000 Property)$35,100

Refund Strategy ImpactReduced to $27,000

The primary hurdle in the Nairobi market is rarely the monthly serviceability of a loan, but rather the initial capital outlay. According to Rehani Soko market intelligence, the standard down payment requirement for non-resident mortgages sits firmly at 20%. For a typical 2-bedroom apartment in Kilimani, priced at roughly $140,000 (KES 18.2M), this demands an upfront cash injection of $28,000.

However, the financing environment is shifting. While the Central Bank of Kenya (CBK) maintains a watchful eye on inflation, dollar-denominated mortgages currently offer significantly more attractive terms for diaspora earners compared to Kenya Shilling facilities. By deploying a substantial tax refund directly into your closing costs or deposit, you drastically reduce the "cash-to-close" friction that stalls many transactions.

The following breakdown illustrates how applying a standard $12,000 diaspora tax refund alters the entry barrier for a Nairobi investment property.

This strategic allocation reduces your immediate financial burden by nearly 34%. To explore specific lender rates that align with this strategy, you can get a mortgage quote tailored to your income profile. For those unsure about the legal nuances of using foreign funds for Kenyan down payments, we recommend consulting our AI assistant at Ask Hani to ensure full compliance with KRA regulations.

Non-Obvious Capital Tips

While many investors view their March tax refunds as "bonus money" for vacations, smart capital allocators treat this liquidity event as the cornerstone of their next acquisition. However, simply having the cash isn't enough; how you structure your entry determines your long-term yield. The critical insight is that your tax refund should not just fund the deposit—it must also cover the "hidden" closing costs that often derail transactions at the eleventh hour.

According to Rehani Soko market intelligence, successful diaspora investors frequently practice "capital stacking." This involves combining your March tax refund with January/February Sacco dividends, which are often paid out early in the year by Kenyan cooperatives. This strategy effectively bridges the gap for the standard 20% down payment required by most lenders. For a standard $115,000 (KES 14.9M) 2BR apartment in Kilimani, the down payment sits at $23,000. If your refund covers $8,000, you are nearly 35% of the way there immediately.

You must also account for statutory costs to avoid liquidity crunches. The Kenya Revenue Authority (KRA) mandates a 4% Stamp Duty on property transfers in municipalities, a figure that cannot be financed and must be paid in cash.

Beyond the acquisition costs, the math justifies the initial cash outlay. Consider the performance of that same unit in a high-demand area.

Projected ROI Calculation:

- Asset: $115,000 2BR Apartment in Kilimani

- Revenue: $1,300/mo (Conservative Airbnb occupancy)

- OpEx: $400/mo (Service charge, cleaning, utilities)

- Net Operating Income: $900/mo = $10,800/year

- Cap Rate: $10,800 / $115,000 = 9.4%

Impact of $12,000 Tax Refund on Capital Requirements

💰Property Price

Standard Cost (USD)$140,000

Out-of-Pocket with Refund (USD)$140,000

💰Down Payment (20%)

Standard Cost (USD)$28,000

Out-of-Pocket with Refund (USD)$16,000

💰Stamp Duty (4% of value)

Standard Cost (USD)$5,600

Out-of-Pocket with Refund (USD)$5,600

💰Legal & Valuation Fees (~1.5%)

Standard Cost (USD)$2,100

Out-of-Pocket with Refund (USD)$2,100

💰Total Cash Required

Standard Cost (USD)$35,700

Out-of-Pocket with Refund (USD)$23,700

This 9.4% return significantly outperforms standard savings accounts, making the deployment of your tax refund a logical financial move. To see exactly how your specific refund amount impacts your borrowing power, you can get a mortgage quote in minutes. If you are unsure about the specific tax implications or KRA requirements for your situation, simply ask our AI assistant at Tangaza to clarify the latest regulations.

Your Next Move

The convergence of tax refund season and the current stabilizing shilling presents a rare window for strategic entry into the Nairobi market. For the diaspora investor, this liquidity event isn't just about extra cash; it is the bridge between intention and asset acquisition. Rehani Soko market intelligence indicates that properties in high-demand zones like Kilimani and Westlands are seeing a statistically significant correlation between March liquidity injections and Q2 price hardening. Waiting often means paying a premium later.

To capitalize on this, you must treat your tax refund as "gap funding." If you are targeting a standard 2BR apartment in Kilimani priced at $135,000 (KES 17.5M), your target 20% down payment is $27,000. Many investors sit with $15,000 to $20,000 in savings, unsure how to bridge the final stretch. Your March refund is that critical missing link. Rather than letting these funds sit in a low-interest savings account, deploying them immediately into a hard asset locks in today's valuation before projected mid-year adjustments.

Below is a precise breakdown of how a typical diaspora tax refund completes the capital stack for a Nairobi acquisition.

Action is the differentiator between an observer and an owner. Do not guess your eligibility. Use our mortgage calculator to see exactly how your new down payment total impacts your monthly rates. If you have specific questions about structuring this capital from abroad or need clarity on KRA compliance for the transaction, Ask Hani immediately. The market moves on data, not sentiment—ensure your capital is positioned to perform.

1. The Math of the Down Payment: Making Your Refund Work

The standard deposit for a mortgage in Kenya typically ranges between 10% and 20% of the property value. For a diasporan looking to reconnect with their roots, this initial capital requirement often feels like the steepest climb. However, when you combine a tax refund with existing savings, that 20% threshold becomes immediately accessible.

Initial Capital Breakdown for $115,000 2BR in Kilimani

💰Down Payment (20%)

Estimated Amount$23,000

Payment TriggerSigning of Sale Agreement

💰Stamp Duty (4%)

Estimated Amount$4,600

Payment TriggerTransfer of Title (Payable to KRA)

💰Legal & Valuation Fees

Estimated Amount~$2,300 (approx. 2%)

Payment TriggerDue Diligence Phase

💰Total Liquid Cash Required

Estimated Amount$29,900

Payment TriggerBefore Handover

According to Rehani Soko property analytics, the entry point for a premium 1-bedroom apartment in high-demand areas like Kilimani or Westlands currently sits between $80,000 and $120,000 (KES 10M - 15M). A 20% deposit on the lower end of this spectrum is $16,000. If your combined household tax refund is $5,000 to $8,000, you have effectively covered nearly half of your down payment in one stroke.

Data Source: Rehani Soko Market Data (2026)

This approach minimizes the need to liquidate other long-term investments, preserving your broader portfolio while securing a tangible foothold in Kenya.

2. Neighborhood Analysis: Where to Deploy Capital

Choosing the right location is critical. You want an area that offers not just capital appreciation but also reliable rental yields if you plan to lease the property. Rehani Soko market intelligence indicates that areas with high expatriate populations and proximity to business hubs continue to outperform the broader market.

We see a clear divergence in performance based on infrastructure developments. Westlands continues to command premium rents due to the expressway connectivity, while Kilimani offers a dense, vibrant rental market. For those seeking long-term family homes, Karen remains a stable, albeit higher-priced, enclave.

Note: Prices reflect properties in Nairobi listed on Rehani Soko.

3. Financial Viability: A Real-World ROI Scenario

Let’s move beyond abstract percentages and look at the hard numbers. The critical insight is that dollar-denominated rental income provides a hedge against local currency fluctuations, a key consideration for diaspora investors.

Capital Stack for $135,000 Kilimani Apartment

💰Existing Savings

Amount (USD)$18,500

% of Purchase Price13.7%

StatusLiquid / Ready

💰Tax Refund (March)

Amount (USD)$8,500

% of Purchase Price6.3%

StatusInjected Capital

💰Total Down Payment

Amount (USD)$27,000

% of Purchase Price20%

StatusSecured

💰Mortgage Balance

Amount (USD)$108,000

% of Purchase Price80%

StatusFinanced

💰Est. Closing Costs

Amount (USD)$7,425

% of Purchase Price5.5%

StatusPaid via Cash Flow

Below is a worked example of a 2-bedroom investment in Kilimani, purchased using a mortgage where the down payment was bolstered by a tax refund.

Worked ROI Calculation: Kilimani 2-Bedroom Apartment

- Purchase Price: $130,000 (Approx. KES 16.2M)

- Down Payment (20%): $26,000 (Partially funded by refund)

- Financing: $104,000 Mortgage

- Gross Income: $1,500/month (Short-stay/Airbnb model)

- Operating Expenses: $400/month (Service charge, utilities, management)

- Net Operating Income: $1,100/month ($13,200/year)

- Mortgage Payment (Est): $850/month

- Cash Flow: $250/month positive cash flow

- Cash-on-Cash Return: ($3,000 annual cash flow / $26,000 invested) = 11.5%

Note: This excludes potential capital appreciation, which historically tracks above inflation according to the Central Bank of Kenya (CBK) data.

4. The Execution Plan: From Refund to Keys

Timing is everything. With your funds arriving, you must act decisively to secure the best units before the post-tax season rush. The process requires navigating legal due diligence, valuation, and mortgage approval.

Down Payment Composition Analysis

💰1BR Apartment

Avg. Price (USD)$90,000

20% Deposit Required$18,000

Refund Contribution ($7k Avg)38.8%

Remaining Cash Needed$11,000

💰2BR Apartment

Avg. Price (USD)$135,000

20% Deposit Required$27,000

Refund Contribution ($7k Avg)25.9%

Remaining Cash Needed$20,000

💰3BR Apartment

Avg. Price (USD)$200,000

20% Deposit Required$40,000

Refund Contribution ($7k Avg)17.5%

Remaining Cash Needed$33,000

According to the Law Society of Kenya (LSK) guidelines, legal fees usually cap at around 1-2% of the purchase price, and Stamp Duty is set at 4% for urban properties by the Kenya Revenue Authority (KRA). Factoring these closing costs into your budget is essential to avoid last-minute liquidity crunches.

Visual summary: The classroom comic below walks through the concepts in this article.

📖

Page 1 of 2Hani Explains It

Actionable Next Steps

Ready to turn your tax refund into a permanent address in Nairobi? Follow this exact path:

- Assess Your Affordability: Use our tools to see what you can afford.

- Verify the Market: Don't just take our word for it; analyze the listings.

- Get Expert Answers: If you are unsure about legal structures or specific diasporan banking needs, ask our AI assistant.

Key Takeaways

- Timing is Key: March liquidity offers perfect timing to lock in pre-construction prices before mid-year adjustments.

- Strategic Allocation: Use the 70/20/10 rule (Down Payment/Costs/Reserves) to maximize the impact of your refund.

- Data-Driven Choice: Focus on high-yield zones like Westlands or Kilimani where Rehani Soko data shows strong rental demand.

- Currency Advantage: For diaspora investors, the current exchange rate amplifies the purchasing power of USD/GBP tax refunds.

- Professional Guidance: Always verify property clean titles and tax compliance through established platforms.

Frequently Asked Questions

- Generally, you cannot pay directly in foreign currency for the final transaction if the vendor requires Kenya Shillings (KES), but many developers and sellers in the premium market accept USD. However, under Central Bank of Kenya (CBK) regulations, anti-money laundering (AML) checks will apply to large transfers. The most efficient method is to transfer your refund into a Diaspora Account held with a Kenyan bank or a specialized mortgage provider. This ensures your funds are recognized as legitimate investment capital. Using a platform like Rehani Soko simplifies this, as we can guide you toward lenders and developers who facilitate multi-currency transactions, ensuring you don't lose value on unfavorable exchange rate spreads during the conversion process.